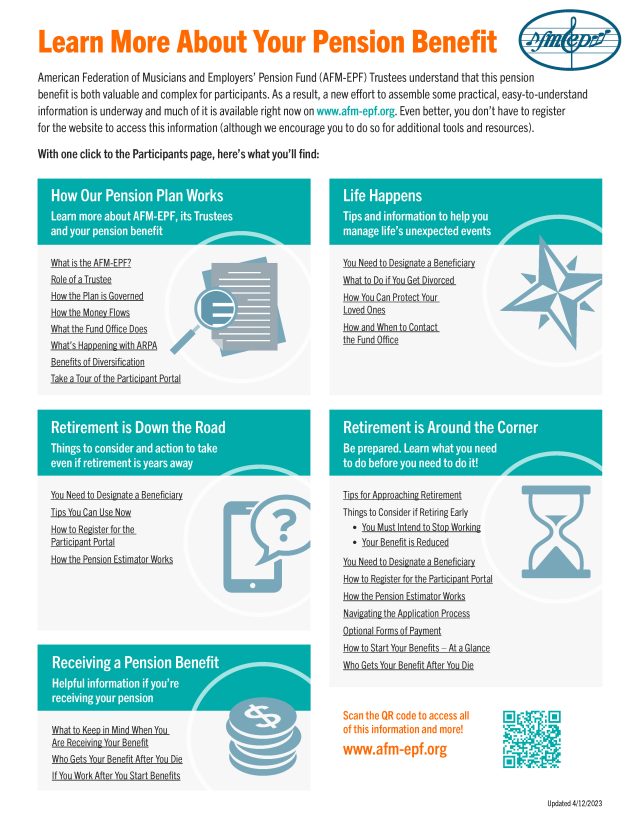

American Federation of Musicians & Employers’ Pension Fund (AFM-EPF) Click here to download a high-resolution PDF version of the graphic above