Allegro

Retirement at Risk

Organizing Matters

Volume CVIII, No. 5May, 2008

May is Labor History Month. In that context it is appropriate for this column to point out some important measures of what the struggle by unions has produced and contrast those events with the current economic landscape.

In the 1950’s and 60’s, hundreds of strikes and thousands of union contracts were settled by starting and improving union pension plans. Those efforts were so widespread that providing a defined benefit pension became something companies did simply because most companies did. These gains have had a long-term payoff in the increasing income available to retirees.

In 1965, two-thirds of Americans over 65 had incomes below the poverty line. Two factors changed this: the doubling of Social Security benefits in the Great Society years in the mid-60’s, and the widespread successful negotiation of pension plans by unions.

Employers subsequently added pension benefits for many others in an effort to keep unions from seeming too attractive and spurring further organizing by unions. Our pension fund, the AFM-EPF, started during this era.

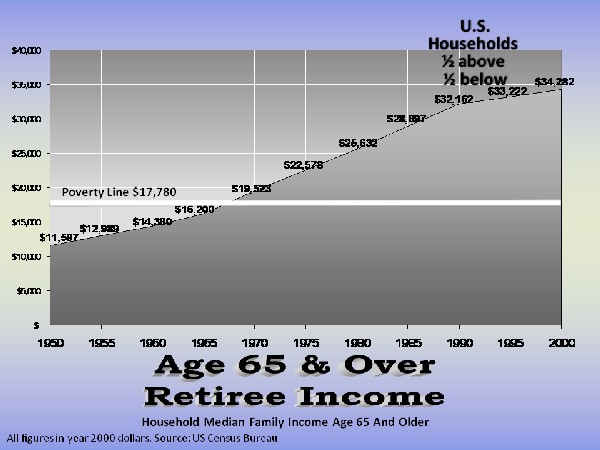

Click chart for full screen version. |

The long-term payoff can be seen in the chart to the right, which illustrates the rise in income for older Americans over the last 50 years. The figures are all expressed in year 2000 dollars so there is a consistent yardstick for comparing year to year, factoring out the effects of inflation over the long term.

The same two factors at work in 1965 are in play today.

The first is Social Security. Payments are declining compared to pre-retirement income. Many more two-earner households don’t get as much replacement income from Social Security because Social Security provides a 50 percent survivor benefit in a double-earner household. The effect of this is that only to the extent that the second income earner receives more than half the income of the higher earner will benefits increase over a lifetime.

The second factor is the tremendous decline in the number of participants in defined-benefit pension plans. Economists at Boston College write, “401k’s and similar plans simply do not pay as well as defined-benefit pensions. In other types of plans people are in charge of their own investments and they make mistakes all along the way.”

Most Americans are not preparing for retirement in any meaningful way. As a result, according to financial writers, there are upwards of 150 million people who face bleak times in retirement. That means the line in the chart will go down in future years. That’s what may be most meaningful to working nonunion: giving up your future income security.

Unions have lost market share, sliding from 35 percent of the workforce in the late 1950’s to 12 percent today. The result is the lessening of the ability to defend gains and a disappearance of the ability to lead the employment market for nonunion jobs.

Another result is a severe decline in the retirement prospects for a majority of employed Americans and small business owners. The run-up in home values is nearly entirely offset by the rise in mortgage debt and the decline in long-term interest rates. The collapse of labor organizing law enforcement under the leadership of successive conservative governments severely retards the gains possible in pensions for new industries.

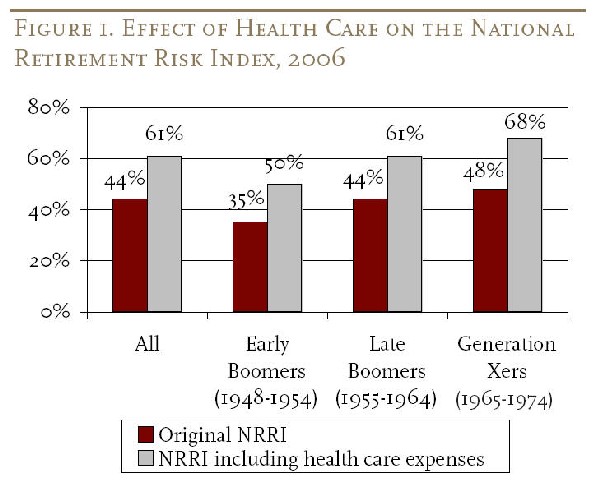

Comparing 1983 and 2005, the number of people at risk of being unable to continue their lifestyle has increased by nearly 80 percent when the cost of health care is factored into the numbers.

The Boston College Center for Retirement Research is an economics institute that has produced a statistic each year since 1983 called the National Retirement Risk Index. Basically, it is a measure of the ability of households to maintain their standard of living in retirement. The economists analyze American household income, employment and census data. They divide up households into the top, middle and bottom thirds by income levels.

Nearly two-thirds of the U.S. households that make up the middle third by income will be forced to live on less than 70 percent of their pre-retirement income when they retire. Nearly half of the households in the top third by income are “at risk” by this measure

Click chart for full screen version. |

The economists at the Center for Retirement Research then broke down the risk to populations by age. (See chart at right.)

By far the greatest increases to being at risk are the young. The economists identified the major reasons for a 40 percent increased risk for the young in the labor force as the replacement of defined-benefit pensions by employers with 401k or 403b personal savings plans, which do not pay as well as defined-benefit pensions for people with increased life expectancies.

(To see the complete study, go to http://ccr.bc.edu. Click on “Publications” from the left-hand, black menus. Then select “Special Projects” and “National Retirement Risk Index.”)

These are sobering statistics. In the not-too-distant future most retirees will be poor — like most retirees were in 1965. That should make all of us aware of how important building a pension benefit is.

To learn more about your pension, check out Local 802’s online seminar: