Allegro

The Political Economy of Collective Bargaining: Health Care

Volume CIX, No. 2February, 2009

The function and purpose of every union is to act in the interests of its members. To put it another way, the purpose of the union is to secure respect. Respect for the members’ time in the form of good wages and paid time off as well as for the provision of income during periods of sickness and unemployment. Respect for the members’ bodies in the form of safe working conditions and good health care for the entire family. Respect for the protection of dire poverty in old age. Respect for the spirit of the community in the form of good education and religious tolerance. Respect for our families’ needs to live free from fear and prejudice in decent homes.

One aspect of the fight for respect is the focus of this report: health care.

Throughout the first half of 20th century America, collective bargaining agreements in the unionized sectors of the economy enforced favorable conditions and gave nonunionized employers an incentive to incorporate union-like wage scales, benefits, and working conditions as normal components of their operations.

The ability of organized labor to win mandatory health insurance for workers at a national level, however, remained elusive.

As historian Jeremy Brecher states, “…by 1935, only about 2 million were covered by private health insurance plans, and on the eve of World War II there were only 48 job-based health plans in the country.”

Meanwhile, faced with intense opposition from medical practitioners and their affiliated organizations — like the American Medical Association, who denounced group insurance as “socialized medicine,” and amidst internal disputes regarding the most effective means of action, labor unions lacked the power needed to achieve its goal until the beginning of World War II.

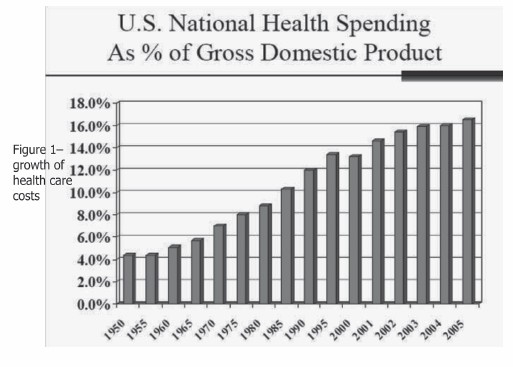

Figure 1. Click to enlarge. |

To support the war effort and normalize industrial relations, a tripartite institution composed of labor leaders, government officials and business elites was named to the National War Labor Board. In addition to its duties of regulating wage and price increases, the body gave employers tax subsidies to provide health insurance to their employees. Congress agreed to make the exemption permanent and that was the takeoff point for employer based health care plans.

Health care started as a small piece of the nation’s spending, measuring just under 4 percent of GDP, when the permanent tax treatment of health plans changed in 1946. Health care today is a gigantic multi industry enterprise accounting for 17.1 percent of GDP. (See figure 1.)

Health care spending in the U.S. in 2007 was $2.17 trillion. The main driver of industrial disputes in union contract negotiations over the last 20 years has been health care costs. Regardless of whether workers were in a plan maintained by the employer or a plan run by the union, finding the money at the bargaining table to cover the increasing costs has been the cause of the vast majority of major strikes in the nation.

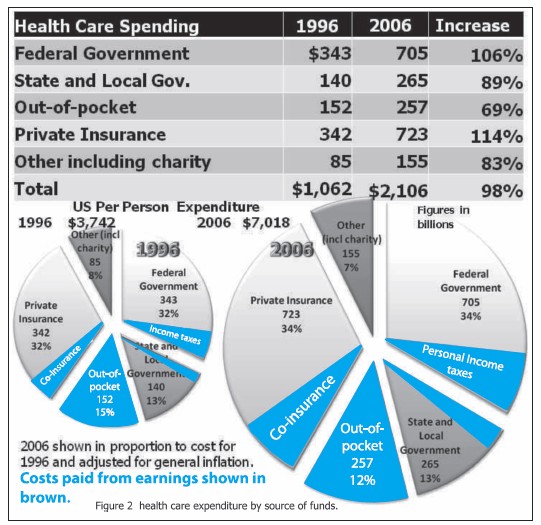

Figure 2. Click to enlarge. |

Figure 2 illustrates how health care costs were paid in 1996 and how costs were paid in 2006. The table at the top shows the percentage growth in the share of costs borne by individuals, insurance plans and governments. Those with the most money paid the most amount of increase. Insurance companies’ payments rose 114 percent while individuals, the least able to pay, saw an increase of 69 percent. The federal government saw its expenses rise by 106 percent during the same period. The federal government was able to pass on cost increases in many instances in the Medicaid program to less powerful states and local governments whose costs rose over 89 percent in the period. State and county governments complain bitterly about “unfunded mandates” but federal requirements prevail.

How to deal with the double-digit annual increases of the cost of health insurance has been the cause for major consternation for bargainers on all sides of the negotiating table for years. There’s an adage among bargainers: “a buck is a buck.” That means that a dollar spent to accomplish one goal at the negotiating table is not available to be spent a second time.

The way most companies have dealt with the cost increases is to push costs onto employees at a pace well above inflation, and to provide less generous coverage (cut back the amount of care).

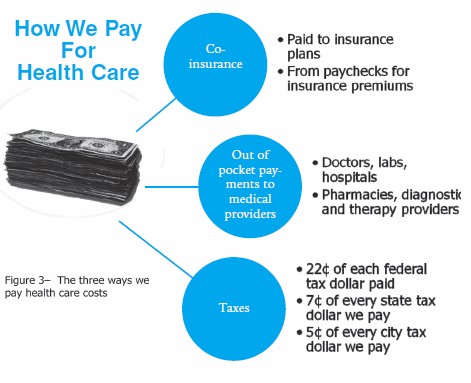

Figure 3. Click to enlarge. |

Employers have the power to drive the cost onto employees three ways. The diagram at the right (figure 3) shows the three ways workers pay for health care:

1. Employees have to pay part of the insurance premiums (now an average of 17 percent for individuals and 26 percent for family coverage).

2. Employees get less insurance coverage for the money — they pay higher deductibles and co-pays and their plans restrict where coverage is in effect

3. Employers use strategies that remove health care from production costs. America’s largest employer, Wal-Mart, forces the financing of employee health care costs onto the public purse. By having a mostly part-time workforce, keeping wages very low, and selling mainly imported goods, the retail giant — with 1.6 million employees — effectively raises taxes for everyone through the amount the government spends on healthcare on those employees. In 2006, 22 cents of every federal tax dollar went to cover health care costs.

Let’s look at these three items in detail.

The first is the most obvious — require employees to pay premiums, or so-called employee co-insurance. This portion has grown to a national average of 17 percent of individual premiums and 26 percent of the rate charged by the insurance companies for family coverage. The annual rate of increase in the last 10 years is 9.3 percent while average inflation was just 2.6 percent.

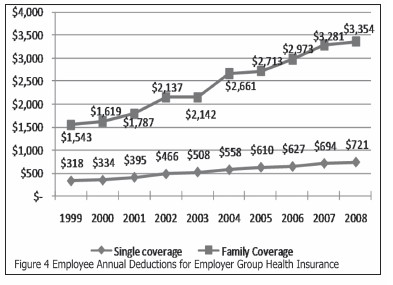

Figure 4. Click to enlarge. |

A few large companies started co-payment of insurance premiums to push cost onto employees. Figure 4 illustrates the growth of employee premiums. The average monthly family plan premium was $280 per month in 2007.

The insurance industry also invented insurance plans that cover fewer services for employees by moving costs onto the insured patient. Whittling away what is covered lowers premium increases for employers. A $10 copayment has become $20 at a minimum — even up to 50 percent of medical service charges.

The type of plan employees are in has changed as well. Conventional plans that covered all services used to cover 73 percent of all employees in 1988. Today those plans cover fewer than 2 percent. Less costly HMO’s and preferred provider organization (PPO) health plans now cover 78 percent of employees. These kinds of plans were only 27 percent of the marketplace in 1988.

Figure 5. Click to enlarge. |

What happens in union bargaining is that the employer talks about “market conditions.” Employers will typically insist that those conditions, or something very close to those conditions, is the only possibility for the framework of an agreement.

Employers do this over and over in the hundreds of negotiations that occur. That slowly forces “market conditions” onto unionized workforces. And nonunion workers just get the cheaper plans at the drop of a memo — no discussion, no appeal. “Don’t like it? There’s the door.”

The bottom line? Union health plans are a firewall. They delay employer efforts to push costs onto workers.

The next article in this series will examine how the dramatic rise of health care costs has impacted union negotiations. We’ll also examine the consequences for your pocketbook in the form of tax increases. Finally, we’ll look at the role of the insurance industry, examine the increased social cost of having 46 million people with no health insurance, and survey the standard comparison points to other developed countries around the world.

SOURCES

- Brecher, Jeremy. “Doctor Wall Street: How the U.S. Health care System Got so Sick.” June 2008. Dec. 2008 http://zcommunications.org/FCKFiles/file/PDFs/DrWallStreetPamphlet.pdf.

- Clemmitt, Marcia. “Universal Coverage: Will All Americans Finally Get Health Insurance?” CQResearcher 17 (2007): 265-88.

- Employer Health Benefits 2008 Annual Survey. Sept. 2008. Kaiser Family Foundation. Dec. 2008 http://ehbs.kff.org/pdf/7790.pdf.

- Health Care Costs: A Primer. Aug. 2007. Kaiser Family Foundation. Dec. 2008 http://www.kff.org/insurance/upload/7670.pdf.

- “Hisotrical Tables: Budget of the United States Government.” 2008. Executive Office of the President of the United States. Dec. 2008.

- Hummelstein, David, and Steffie Woolhandler. “Medicine as Industry: The Health Care Sector in the United States.” Monthly Review Apr. 1984: 13-25.

- Mason, J. W. “Health and Social Services.” 4 Dec. 08. NY Independent Budget Office. 4 Dec. 08 http://www.ibo.nyc.ny.us/.

- New York State 2009-2010 Executive Budget. New York State Division of the Budget. Dec. 2008 http://publications.budget.state.ny.us/eBudget0910/ExecutiveBudget.html.

- Rodberg, Leonard. Who Needs Insurance Companies Anyway? Physicians for a National Health Care Program. Dec. 08.

- Single Payer FAQ. Physicians for a National Health Program. Dec. 08 http://www.pnhp.org/facts/singlepayer_faq.php.