Allegro

What’s in Obama’s Health Plan for Us?

Volume CX, No. 5May, 2010

Photo: Leoncillo Sabino via Flickr.com |

Many Americans watched and wondered if a health care overhaul would pass Congress. In March it finally did.

The Patient Protection and Affordibility Act was signed by President Obama on March 23, and the Health Care and Education Affordibility Reconciliation Act was signed on March 30.

Now what? Many people are wondering how this new law will affect them. The short answer is, probably not much, at least for a while.

However, there are aspects to the bill that may eventually help Local 802 members quite a bit.

Exchanges

For instance, let’s say you don’t do enough union work to get on the union’s health plans. If you want health insurance right now, you have to buy it out of pocket, or apply for Medicare or Medicaid (if you’re eligible) or appeal to the many low-cost or charity care services for artists and others that exist in this area.

But, starting in 2014, those who don’t have health insurance can buy it through new, so-called “exchanges.”

The exchanges will be run either by the states, the federal government or by nonprofit entities. Insurance companies will market their products on the exchanges.

Federal regulation will mandate a certain level of benefits to prevent the companies from offering “swiss cheese” policies, meaning policies with a lot of holes – services not covered or very high out-of-pocket expenses. They will also be barred from cherry picking only healthy individuals.

The exchanges will be set up in a way to make it easier for people to read and understand what is covered and how much everything will cost.

Timeline

The laws are designed so that various aspects of health care reform roll out in pieces over the next 10 years. So here is a timeline of how the new health care provisions may affect you.

2010

- If you are uninsured and in bad health you can get coverage through a high-risk pool. (This has already been true if you live in Connecticut, and if you live in New Jersey or New York, insurance companies already cannot deny coverage for this reason, though currently they can make you wait 12 months to get your illness covered.)

- Your dependents up to age 26 must be allowed to enroll in your group plan if they have no coverage of their own, either by September of this year or when your current union contract expires, whichever is later. (This has already been true in Connecticut; in New York it is up to age 29 and in New Jersey it is age 30. Because Local 802’s plan is “self-insured,” it has not been subject in the past to the New York law.)

- If you run a small business of 25 or fewer employees, you can get a tax credit for covering them.

- If you are on Medicare Part D and you hit the “doughnut hole,” you will get a rebate of $250. (If you’re on Medicare now, then you probably know what the “doughnut hole” is. If not, e-mail me and I’ll go over it with you.)

2011

- If you hit the Medicare doughnut hole (see above) you will get a 50 percent subsidy for brand-name prescriptions. New long-term care policies will be available to help disabled people stay in their homes or to help with nursing home care.

- Employers will begin reporting the value of your health benefits on your W-2.

2013

- Tax-free contributions to flexible spending accounts will be capped at $2,500 annually.

- Medicare payroll tax on individuals earning $200,000 a year ($250,000 for couples) rises to 2.35 percent from 1.45 percent. Also, these individuals will pay a new 3.8 percent tax on dividends, the first Medicare tax ever on investment income.

2014

- Plans may not impose restrictive yearly caps beginning Jan. 1, 2014, or when your union contract expires after that. This will most affect people on Local 802’s Plan A ($50,000 cap) and Plan B ($5,000). We will not know exactly how these provisions apply to our plan until the U.S. Department of Health and Human Services writes regulations.

- Nonprofit exchanges will be established with private health plans offering at least two levels of coverage. Benefit levels will be federally mandated and deductions will be capped at $2,000 for an individual and $4,000 for a family.

- Insurance companies will be barred from denying coverage to anyone with health problems and also barred from dropping such people. (This is already the law in New Jersey and New York).

- Group plans must offer to enroll dependents up to age 26, even if they do have their own coverage.

- Subsidies to help pay premiums available for people up to 400 percent of federal poverty level, about $88,000 for a family of four. The subsidies are aimed at ensuring that you do not pay more than 8 percent of your income for premiums.

- Families at 133 percent of federal poverty level (about $29,300 for a family of four) will be eligible for Medicaid.

- Everyone will be required to carry health insurance. $95 a year for non-compliance in 2014, rising to $750 by 2016, then indexed to inflation. The fines are capped at $2,250 for a family.

2018

- A so-called “Cadillac tax” will be imposed on plans whose costs exceed $10,200 a year for an individual and $27,500 a year for a family. The tax is 40 percent on the amount above those values. This tax is very unlikely to apply to the Local 802 plan, though costs that far into the future are unknown.

2020

- The Medicare Part D “doughnut hole” closes completely (see my notes for year 2010, above). Seniors responsible for 25 percent of their prescription costs.

Conclusion

What I like about the health care reform bill is that it may force insurers and the government to demand better value from the providers.

Right now the insurers are at war with the providers.

The providers want to keep charging more and more for their services They buy more and more hardware, MRI machines, real estate, you name it, and they need to recover their investment plus make a profit. So that means that if there are three CT scanners, all three are booked all the time.

Because most insurance plans pay fee-for-service, the incentive for providers is to do more and more tests to make more and more money.

And this is one major reason why all of our insurance premiums are rising at such a dizzying rate.

The insurance companies, often clumsily, are trying to control that runaway cost curve. The problem is, they often use a blunt instrument, rather than making good medical choices. That is the war. Not much room for the patient, is there?

In fact, patient outcomes are not particularly good in the U.S. compared to other developed countries, meaning that we are not getting good value for our dollars.

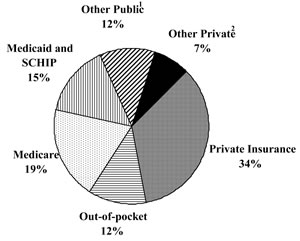

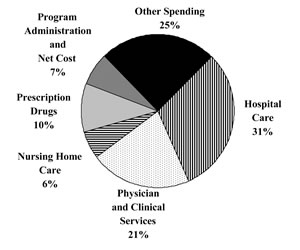

If you look at the pie charts below, you can see where the money came from and how it is spent.

An underreported aspect of the health care reform bill is the pages and pages of pilot programs.

One of them is simple: put doctors on salary instead of paying them for each procedure.

Others include: experimenting with bundled payments and comparative research, compelling medical device companies to prove the worth of their products and generally finding ways to get better quality rather than quantity.

Over 30 years of research shows we can save about a third of what we spend if we insist on quality rather than quantity. Perhaps these programs will help lay the groundwork for additional reforms.

|

The nation’s health dollar: where it came from |

|

|

The nation’s health dollar: where it went |

|

| “Other Spending” in the bottom chart includes dentist services, other professional services, home health, durable medical products, over-the-counter medicines and sundries, public health, other personal health care, research and structures and equipment. For additional notes and souces for both charts, e-mail allegro@local802afm.org | |