Allegro

Can the pension fund get better returns?

Volume 117, No. 4April, 2017

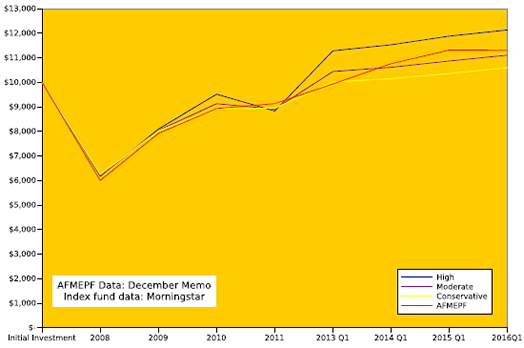

This is a follow-up to my column in the March issue of Allegro and President Tino Gagliardi’s response. President Gagliardi feels that the 25 investment firms hired by the fund do better than an investment in an index fund. To test this, I prepared a basket of index funds, diversified across bonds, real estate and stocks. The stock funds represent large and small cap, U.S. and international. The exact funds do not matter, since any equivalent basket of index funds would have performed the same, but I am happy to provide these on request. Figure 1 below shows three versions of these funds, from high to medium to low volatility, along with the funds’ performance.

Figure 1: Where’s the sizzle? CLICK IMAGE TO VIEW LARGER SIZE (This chart provided by a Local 802 member. Local 802 takes no position on the validity of this chart or any data therein.)

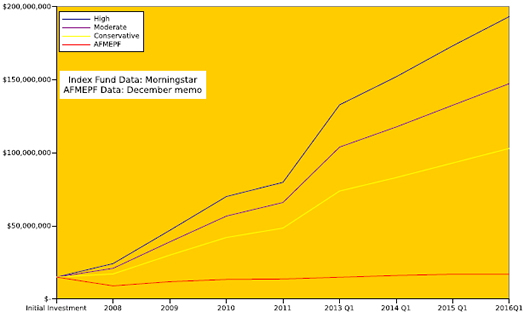

As you see, the AFM pension fund’s performance (indicated by the red line) is the same as the indexed funds. The trustees pay about $11 million a year for investment sizzle, but where’s the sizzle? The sad reality of this performance is that we could have had the same results by setting a match to $11 million dollars a year and investing the remainder in indexed funds. But this is not the entire story. The total amount lost to members is not just the $11 million each year. That $11 million could have been invested and would have compounded over the following years, delivering value to the members. Figure 2 below shows how much we have lost. This is the additional value lost over that period by not investing into a diversified basket of index funds.

Figure 2: The true cost of fund managers vs. index funds. CLICK IMAGE TO VIEW LARGER SIZE

(This chart provided by a Local 802 member. Local 802 takes no position on the validity of this chart or any data therein.)

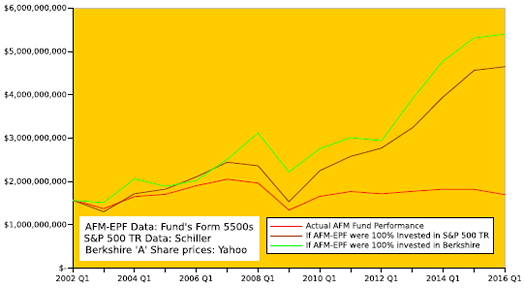

Even this is not the entire and sad story of the fund’s investment performance. Figure 3 below illustrates what would have happened to the fund under two alternative scenarios. The actual AFM pension fund performance is indicated by the red line. Scenario 1 is to invest all the fund’s assets into the S&P 500, with dividend reinvestment, indicated by the brown line. (“TR” stands for “total return.”) Scenario 2 is to invest all the funds assets into Berkshire Hathaway (indicated by the green line). I used the fund’s income statements from 2002 to 2016 (fiscal year end dates), amortizing these amounts over the 12 month fiscal year to get as close as I could to a realistic simulation.

Figure 3: Two “What If” scenarios. CLICK IMAGE TO VIEW LARGER SIZE

(This chart provided by a Local 802 member. Local 802 takes no position on the validity of this chart or any data therein.)

What I find compelling and fascinating about this chart is not how much better the S&P500 TR index has done, or even how much better Warren Buffett has done. What fascinated me when I first saw these curves is how much better the fund did prior to 2009 than it has done since. Prior to 2009, the fund did a fairly decent imitation of the S&P500 TR. If it had continued that style of performance post 2009, it is my belief that we would all be quite happy today. But the fund has not even matched its own previous performance. This should have been obvious to the trustees as early as 2010, but if not by then, certainly 2011 or 2012. This is a hard question, but I believe it is a fair and reasonable one: Why did the trustees fail to see the sinking investment ship? Or if they did, why did they fail to correct it? Of all the many suggestions to correct the fund’s problems, better monitoring of investment performance must be at the top.

I will close with a few comments on the investment management style at the fund. Our investment advisors argue that we are doing “as well” as other pension funds. I wonder if these same advisors would be comforted to hear that, while their child received a “D” on their report card, he did as well as other “D” students? If the trustees have accepted this as their metric, they should abandon it post haste. President Gagliardi argues that active management can out-perform passive indexing. I completely agree, but to my knowledge, there is not a single example of outstanding investment management performed by 25 investment managers. In fact, the results of such a crowd are, thanks to the mathematics of the bell curve, most likely to be what we have received: mediocre.

All the great investors of history worked by themselves, or with a partner. This includes Buffett, his teacher Graham, Seth Klarman, Peter Lynch and John Templeton. I would urge our trustees to stop seeking comfort in a crowd of underperforming pension funds, and try to do something better. If there are to be benefit cuts, then there must also be cost cutting at the fund, and a dramatic change in investment performance. I realize that drastic changes take courage. Let us hope that our trustees have an ample supply of that ingredient.

I close with three quotes of John Templeton, one of history’s greatest investors, that I hope our trustees will heed:

- “No committee has ever invested as well as a single person, except by accident.”

- “If you want to have a better performance than the crowd, you must do things differently from the crowd.”

- “If we become increasingly humble about how little we know, we may be more eager to search.”

Local 802 President Tino Gagliardi replies:

Allegro is publishing letters from members – including those carrying on a discussion from previous issues – as a service to our members, knowing that the pension situation is on everyone’s mind. We definitely do not want to stifle reasonable discussion. With respect to the pension fund’s investment strategy, it’s difficult to respond to specific questions or debate the strategy through an exchange in Allegro. Suffice it to say that reasonable and sophisticated investors have long debated active vs. passive management, and we are not going to resolve that debate here. In addition, hindsight is not the appropriate way to measure the prudence of an investment approach, especially because what works in one or more years may not in other years. As stated at the Feb. 22 membership meeting and as I explained in my letter in the March issue of Allegro, the pension fund uses passive management where it is appropriate. The trustees are following what they believe to be a prudent approach with respect to asset allocation and diversification. They continuously review and have reviewed these issues throughout the years. Please keep checking the pension fund’s web site at www.afm-epf.org for more information as it becomes available.

– Local 802 President Tino Gagliardi

More thoughts on our pension fund

I’ve been a proud member of the AFM since 1979. I opened the March issue of Allegro hoping to get the official word on what’s being done to fix our broken pension fund. We’ve all worked so damn hard for the bits of money that (some) of our employers contribute. After 30 or 40 years, if you fall into the right scenes, it can be a nice chunk of change. Traditional fixed pensions are a dying breed, and until relatively recently, ours was in relatively decent shape.

Mr. Ballantyne and Mr. Gagliardi both made valid points in their “Member to Member” exchange. Clearly, the main issue facing our pension fund (and many other pensions) is that more goes out than comes in. But that makes it even more imperative that the current, outdated investment model is, at minimum, revised. Though private equity, hedge funds, commodities, derivatives and real estate are fine in small doses, low-cost index funds and ETFs that mimic the entire market should be the main vehicle to achieve diversification. Pricey, overly complex investment stews concocted by too many chefs are killing – or have killed – so many pension funds.

And it sure as heck doesn’t take 25 people to manage a modern, safe fund. Attempting to beat the market is both irresponsible and expensive. Simplify, avoid high fees and expense ratios, and let the muses have their way. Then we can shut up and play our horns!

–Dan Wilensky

I attended the standing-room only, overflow meeting at Local 802 on Feb. 22, addressing pension fund concerns. And the message is indeed sobering and concerning. Members and fund managers all spoke very respectfully and were well informed. And yes, the financial market’s ebbs and flows play a big role. But as the meeting ended I realized a key component of the problem had not really been articulated. And that is that our “industry” has been shrinking for 20 years. Leaving aside the why’s, wherefore’s and warnings for the moment, the bottom line is that contributions from employers are way, way down, while benefits must be paid. In other entertainment industries, for the most part, to be hired to work in TV and film for example, one must be a member of SAG-AFTRA. Apparently these employer contributions cover the benefits paid out. But too often jobs offered to musicians are non-union. We lost whatever leverage we had at one time to outsourcing, technology and then to a pervasive anti-union rhetoric and groups of musicians working outside the purview of the union. The result of fewer union jobs and musicians not working – or on jobs that pay less with no benefits – is a pension fund in critical status and a struggling union. It’s a vicious cycle. Yes, the fund can look to be better and more frugally managed, but without a revitalized and unionized music industry it will be very hard to reinvigorate the pension fund to its proper status.

–Olivia Koppell