Allegro

Understanding our pension

Part one in a series

Volume 122, No. 8September, 2022

Click to download a PDF with helpful links to our pension fund

By the Local 802 Communications Subcommittee (Deborah Assael, Bud Burridge, Sara Cutler, Martha Hyde, and Wende Namkung)

There has been and still is a lot of confusion over how our pension fund works and how pensions in general work. This series of articles is intended to examine the history of American pensions from the early retirement plans up to the American Rescue Plan Act of 2021.

A pension plan is one way to ensure wealth is carried to the end of a worker’s life, sometimes making it possible for that worker to pass wealth to offspring. Pension plans were not and still are not available to everyone. Private pension plans are often bargained with employers by unions, so a history of American pensions will hew closely to the checkered history of the American labor movement. In that history as in all American history, racism, sexism, elitism and political conflict are marbled throughout. This series will deal mostly with private, defined benefit pensions.

First, a quick primer for our newer members. Our pension plan is officially called the American Federation of Musicians and Employers’ Pension Fund. Every time you play a union gig that includes a pension provision, your employer makes a contribution on your behalf into the fund. Over time, you become “vested” in the pension plan, and when you retire, you may get a guaranteed monthly check. We’ll include more details in the future, but that’s how it works in a nutshell.

Secondly, here are some useful definitions:

Private “defined benefit” pension plan. The AFM pension plan falls into this category. These types of plans are usually bargained between an employer and a union. A prescribed amount of money is paid from a trust fund to the retired worker, usually in the form of monthly payments or annuities. The amount contributed to the fund by the employer varies according to what’s negotiated with the union. These plans are governed by the Employment Retirement Income Security Act and the Pension Benefit Guaranty Corporation.

“Defined contribution” plan. A 501(k) or 403(b) are examples of this type. Pre-tax funds (with set maximum limits on contributions) are deposited into an account for the worker. These funds can be invested in the stock market. Usually both the worker and employer contribute. Upon retirement, the amount paid out is what the account holds, which can vary depending on the market.

Public pension plan. If you’re a city or state worker, your pension may fall into this category. These pension plans are usually a defined benefit pension sponsored by the federal, state or municipal government. Often bargained between a union and the government. Not governed by the Employment Retirement Income Security Act or the Pension Benefit Guaranty Corporation but rather by acts of Congress or state legislatures.

A HISTORY OF PENSIONS IN THE UNITED STATES

Both private employer-provided retirement plans and government-provided pension plans go all the way back to the 19th century. Government-provided defined benefit plans were offered after the Revolutionary War when the new American government guaranteed income for war veterans for the rest of their lives.

In 1875, the American Express Company started the first private pension plan that benefitted disabled, elderly former employees after 20 years of service and after they attained age 60. It was a defined benefit that guaranteed the retiree half his salary per year for life up to an annual cap of $500. In 1880, the Baltimore & Ohio Railroad Company began its own, similar plan. More plans followed, mostly in the railroad, banking and public utilities industries which were largely populated by white, male workers.

In 1886, the American Federation of Labor was established in Columbus, Ohio. Though it didn’t consider itself a whites-only organization, it supported segregated locals and often refused to admit Black locals to its membership. Adhering to its own racist agenda, in 1902, it also argued for the extension of the Chinese Exclusion Act, an 1882 law that prohibited the immigration of Chinese and other Asian workers. In language laced with anti-Asian stereotypes, the AFL insisted these workers undercut white workers because of their alleged willingness to tolerate inferior pay and working conditions.

In 1909, the International Ladies Garment Workers Union, a union populated by mostly female, white, Italian and Jewish immigrants, proved itself a rising power by calling two strikes, one involving 20,000 workers, the other involving 60,000 workers. In the negotiations that ensued, the ILGWU won recognition and, despite the disastrous Triangle Shirtwaist Factory fire and political infighting within the union, it lasted well into the 20th century before merging with two other unions to form Unite HERE. It and several other unions sent a resolution to the floor of the AFL convention in 1935 that would have permitted craft unions (unions that covered workers with specialized skills) to organize large factory workforces. The AFL was not interested in low-skill workers, so the resolution was defeated and the ILGWU went on to help form the Committee for Industrial Organization, though it did return to the AFL three years later. A retiree services department of the ILGWU was formed in 1966 but a defined benefit pension for its largely female workforce came much later than it did for most of their male counterparts in other unions.

In 1921, retirement plans began to take a more formalized shape. The Metropolitan Life Insurance Company offered the first group annuity contracts to cover retirement benefits for workers, These contracts allowed companies to pay premiums on behalf of their workers to the insurance company and the company managed the growth of those monies and paid out either a lump sum or a stream of payments to the retirees. The federal government supported these plans by making the premiums tax deductible.

In 1929, the Great Depression dropped the bottom out of the U.S. economy. The stock market crashed and businesses suffered severe cash shortages. By this time 2.7 million workers — 10 percent of the workforce — were covered by nascent pension plans. Strapped businesses slashed benefits and some terminated the pensions and, because retirees had no benefit guarantee, they suffered the losses.

Recognizing massive poverty among elderly and disabled people, President Franklin D. Roosevelt signed the Federal Social Security Act into law on August 14, 1935. It provided “old age” assistance, disability assistance, public health and child welfare. It was and still is funded by payroll taxes which began in 1937. The first benefits were paid in 1942. Although these benefits were intended to level the economic playing field for millions of Americans, agricultural and domestic workers were not covered, which had the effect of excluding most Black, Asian, indigenous, Latinx and female workers from the new safety net. The benefit was finally extended to those workers in 1950. It also did not cover railroad workers who had their own government retirement plan called the Railroad Retirement Board.

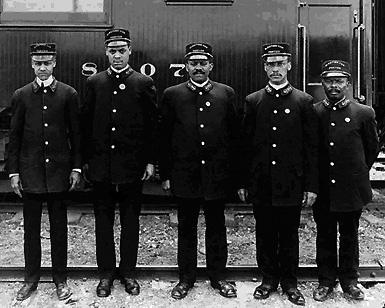

In 1937, the Brotherhood of Sleeping Car Porters, a Black labor union, won its first contract with the Pullman Company after decades of battling the anti-union company and the segregationist AFL which finally recognized and admitted the sleeping car union that same year. The leader of this effort was A. Phillip Randolph, an early activist in the civil rights movement. Shortly after Emancipation, the Pullman Company had a policy of hiring only Black workers as porters. The company saw this new workforce as a source of cheap labor. It exploited them by paying very low wages and requiring long hours. White railroad unions, whose workers had pensions and earned far more in wages, refused membership to Black workers. A defined pension for sleeping car porters likely came much later when they were made participants in the Railroad Retirement Board.

In 1937, the Brotherhood of Sleeping Car Porters, a Black labor union, won its first contract with the Pullman Company after decades of battling the anti-union company and the segregationist AFL which finally recognized and admitted the sleeping car union that same year. The leader of this effort was A. Phillip Randolph, an early activist in the civil rights movement. Shortly after Emancipation, the Pullman Company had a policy of hiring only Black workers as porters. The company saw this new workforce as a source of cheap labor. It exploited them by paying very low wages and requiring long hours. White railroad unions, whose workers had pensions and earned far more in wages, refused membership to Black workers. A defined pension for sleeping car porters likely came much later when they were made participants in the Railroad Retirement Board.

There was a series of laws enacted to protect pension benefits and extend lump sum Social Security benefits to surviving dependents. The new laws required investment advisors to register with the Securities and Exchange Commission, to be licensed by states and to follow regulations designed to protect the investors (like pension funds) whose money they were handling. The Internal Revenue Act of 1938 made pension trusts irrevocable and enacted “non-diversion” rules regulating how plan assets could be used for a company’s benefit when and if its pension was terminated.

A huge game changer came in the form of the Labor Management Relations Act of 1947, also known as Taft-Hartley after its co-sponsors. After World War II there was a wave of strikes, including an extended strike by the United Auto Workers. In 1945 to 1946, 10 percent of the workforce — about 4.6 million workers — struck. There was widespread discontent in the country over the strikes and the new Cold War and there was fatigue over the New Deal. Republicans took over both houses of Congress in 1946 and the LMRA was introduced in the House by Rep. Fred Hartley, Republican of New Jersey and Senator Robert Taft, Republican of Ohio. It passed both houses, and was sent to President Harry Truman, whose veto was overridden. Truman admitted supporting the bill but vetoed it for partisan reasons, knowing Congress had the votes to override. The law prohibits secondary boycotts where a union threatens to penalize an unrelated business for working with an employer with whom the union has a dispute. It prohibits coerced union membership, allowing states to enact right-to-work laws. It forbids “featherbedding” — the practice of requiring employers to pay for more employees than they need.

A huge game changer came in the form of the Labor Management Relations Act of 1947, also known as Taft-Hartley after its co-sponsors. After World War II there was a wave of strikes, including an extended strike by the United Auto Workers. In 1945 to 1946, 10 percent of the workforce — about 4.6 million workers — struck. There was widespread discontent in the country over the strikes and the new Cold War and there was fatigue over the New Deal. Republicans took over both houses of Congress in 1946 and the LMRA was introduced in the House by Rep. Fred Hartley, Republican of New Jersey and Senator Robert Taft, Republican of Ohio. It passed both houses, and was sent to President Harry Truman, whose veto was overridden. Truman admitted supporting the bill but vetoed it for partisan reasons, knowing Congress had the votes to override. The law prohibits secondary boycotts where a union threatens to penalize an unrelated business for working with an employer with whom the union has a dispute. It prohibits coerced union membership, allowing states to enact right-to-work laws. It forbids “featherbedding” — the practice of requiring employers to pay for more employees than they need.

But most significant for pension funds was Section 302 which explicitly forbids an employer from giving money or anything of value to a union. This provision was put in to counter widespread bribery of union officials by employers. The exception to this rule was the Taft-Hartley multiemployer benefit trust fund. Under Section 302, employers in a common industry could pool their contributions to a pension, health or welfare trust fund for the benefit of their employees provided the trust fund was held separately and overseen by a board of trustees with equal representation of employees (union members) and contributing employers. This allowed workers in industries with a lot of employee mobility to accumulate enough credits to enjoy a defined benefit upon retirement for the rest of their lives. Truckers, construction workers, confectionery workers and entertainment workers often move from job to job and this provision allowed all of their collectively bargained work credits to add up to a meaningful pension benefit.

This landmark law, along with the 1950 expansion of Social Security to agricultural and domestic workers, meant that by the mid-20th century an unprecedented number of people had access to a defined benefit pension.

In my next installment, I’ll cover the period 1958 to 2001, including the Civil Rights Movement, the Employment Retirement Income Security Act, the “dot com” bubble, and 9/11.

This article was submitted by the Local 802 Communications Subcommittee, which includes as one of its members Martha Hyde, a trustee on the AFM pension fund. Martha invites members to contact her with general pension questions at earmar4@verizon.net. (Specific pension funds relating to your own pension situation must be directed to the pension fund.)

DID YOU KNOW? The pension plan that covers Local 802 musicians (and all AFM musicians) is called the American Federation of Musicians and Employers’ Pension Fund. At Local 802 and in Allegro, we abbreviate this to the AFM Pension Fund or the AFM-EPF. Want to know more? Watch the movie clip below:

DID YOU KNOW? The AFM Pension Fund is a separate entity from Local 802. Local 802 cannot answer specific pension questions that relate to your pension benefit. For all questions, including your current pension estimate, start here and also watch the movie clip below:

DID YOU KNOW? You can specify a beneficiary to your pension payments in the event of your death before you begin receiving your pension. Want to know more? Watch the movie clip below: